A discounted cash flow (DCF) estimates what a business is worth today by projecting the cash it will generate in the future and discounting that cash back to the present. The logic: a dollar earned years from now is worth less than a dollar today, so future cash flows are "discounted" to a present value. Add them up and you get an estimate of intrinsic value. Here is how it works, in plain English, including the inputs that move the answer the most.

The four steps of a DCF

- 1. Start with free cash flow.Begin from the company's most recent annual free cash flow (operating cash flow minus capital spending), the real cash the business throws off after keeping the lights on.

- 2. Project it forward. Grow that cash flow over the next several years at a chosen growth rate, usually fading to a slower rate as the company matures.

- 3. Add a terminal value. Estimate the value of all cash flows beyond the projection window, growing at a small perpetual rate. This often makes up the majority of the total value.

- 4. Discount everything to today. Bring each future cash flow back to present value using a discount rate (the WACC), then sum them, add cash, subtract debt, and divide by shares to get a per-share intrinsic value.

Why a two-stage model

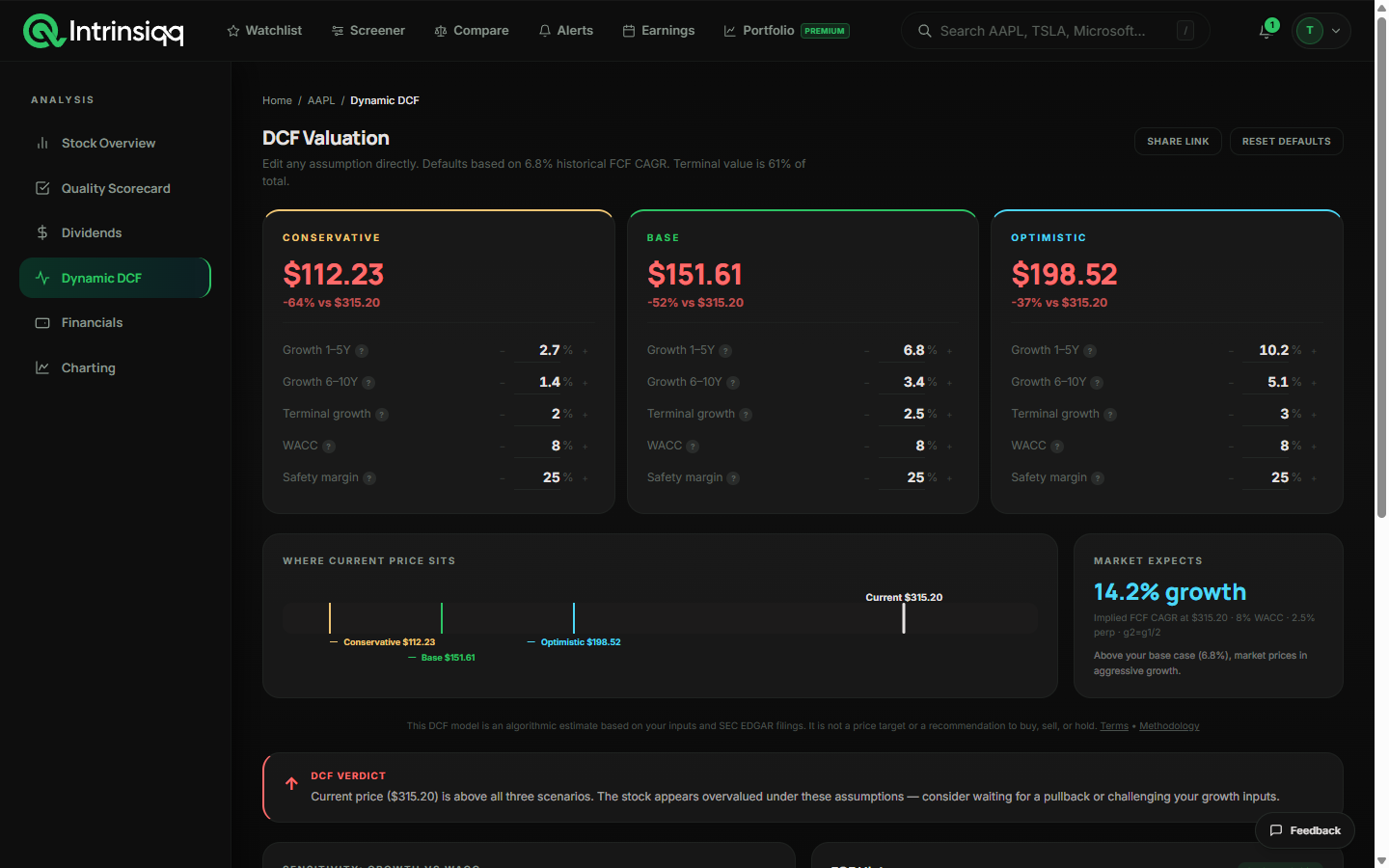

Real companies do not grow at one constant rate forever. A two-stage DCF uses a higher near-term growth rate for the first few years, then fades to a lower rate, which is far more realistic than assuming a single rate. The Intrinsiqq DCF is a two-stage model you can adjust yourself.

The inputs that move the answer

A DCF is only as good as its assumptions, and a few of them do most of the work. This is the table to keep in mind:

| Input | What it is | Effect on the value |

|---|---|---|

| Starting free cash flow | The most recent annual FCF | The base everything else grows from |

| Near-term growth | Growth for the first stage (e.g. years 1-5) | Higher growth, higher value; be conservative |

| Fade growth | Slower growth for the later stage | Bridges high growth to maturity |

| Terminal growth | Perpetual growth after the window | Small changes have an outsized effect on the total |

| Discount rate (WACC) | The required annual return | Higher rate, lower value; reflects uncertainty |

Because everything grows from the starting free cash flow, it is worth seeing how steady that base is. On Intrinsiqq you can chart a company's free cash flow over a decade before you model it forward, so a single flattered or depressed year does not quietly skew the whole valuation.

See a worked DCF on a real stock

Financials pre-loaded from SEC filings; adjust the growth and discount rate and watch the fair value change.

Open AAPL's DCFWhat a DCF can and cannot tell you

A DCF is a disciplined way to connect a price to the cash a business must produce to justify it. What it cannot do is predict the future: garbage assumptions in, garbage value out, and the terminal value in particular can dominate the result. The right way to use it is less "what is the exact fair value" and more "what does today's price assume, and is that believable?" Use it alongside a quality assessment so you are valuing a business you actually understand, and read our guide on telling if a stock is overvalued for how the DCF fits with valuation multiples.